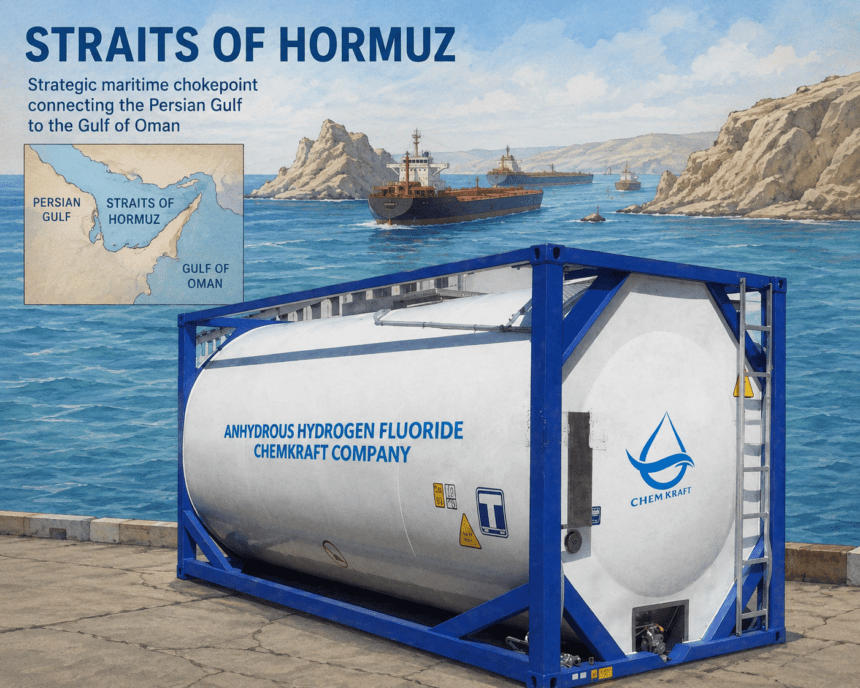

Supply chain disruptions stemming from the ongoing conflict in Iran and the subsequent closure

Supply Chain Mechanics

Anhydrous hydrogen fluoride is essential for etching and cleaning silicon wafers, removing oxide films and metal contaminants during fabrication. The chemical is derived from fluorite and sulfuric acid, the latter of which is produced primarily from sulfur—a byproduct of crude oil and natural gas refining. The war in Iran has severely constrained refining capacity and sulfur supplies, creating a cascading effect through the supply chain. China, the world’s largest exporter of anhydrous hydrogen fluoride, has responded by restricting exports, driving prices up by as much as 130% over early-2026 levels as of mid-April.

Cost Transmission to Memory Makers

South Korean chemical suppliers—including Soulbrain, ENF Technology, and Foosung—began receiving higher-priced orders of scarcer anhydrous hydrogen fluoride in mid-May. These firms blend the material with ultrapure water and ammonium fluoride before supplying it to Samsung and SK Hynix. Industry reports indicate these suppliers will pass on the increased costs to chipmakers by early July. Unlike the 2019 Japan-South Korea trade dispute, which saw minimal consumer price impact due to large memory inventories, the current market lacks such buffers. Global memory supply remains tight, making cost absorption unlikely.

Historical Context and Mitigation Efforts

The 2019 export restrictions by Japan cut 87.9% of South Korea’s hydrogen fluoride supply, forcing diversification toward U.S., Taiwanese, and Chinese sources. While memory prices rose temporarily, they normalized by late 2019. Today’s environment differs fundamentally: there is no oversupply to cushion price increases. However, South Korea has been investing in domestic production capacity. Fluoride Korea, a subsidiary of BGF EcoMaterials, is building a $100 million anhydrous hydrogen fluoride plant in Ulsan with an annual capacity of 50,000 tons—roughly half of national demand. The facility is expected online by Q4 2026, providing a medium-term buffer.

Forward-Looking Conclusion

The impending cost increase for anhydrous hydrogen fluoride represents a material near-term risk for memory pricing, with no immediate relief from existing inventories. While the disruption may be short-lived—given the planned domestic production ramp—the episode underscores the fragility of just-in-time supply chains for specialized semiconductor inputs. Memory makers and their customers should prepare for elevated costs through the remainder of 2026, with stabilization likely only after new domestic supply comes online.